Why Time Series Data Needs To Be Stationary ?

(1) Reason-1

- In Time Series data we know that the current data value is dependent on the previous data values.

- Which means there is a relationship between previous values and current values.

- If the data set is non-stationary the mean and variance of the data will change over time.

- As time series uses only one variable for prediction, with changing mean and variance it will be difficult to calculate the relationship between past values.

- Hence Time Series demands the Stationarity of data.

(2) Reason-2

What quantities are we typically interested in when we perform statistical analysis on a time series? We want to know

- Its expected value,

- Its variance, and

- The correlation between values s� periods apart for a set of s� values.

How do we calculate these things? Using a mean across many time periods.

The mean across many time periods is only informative if the expected value is the same across those time periods. If these population parameters can vary, what are we really estimating by taking an average across time?

(Weak) stationarity requires that these population quantities must be the same across time, making the sample average a reasonable way to estimate them.

(3) Reason-3

- To solve anything we need to model the equations mathematically using statics.

- To solve such equations it needs to be independent and stationary(not moving)

- In stationary data only we can able to get insights and do mathematical operations(mean, variance etc..) for multi-purpose

- In non-stationary, it is hard to get data

- During the conversion process, we will get a trend and seasonality

(4) Reason-4

- Consider the forecasting problem. How do you forecast?

- If everything‘s different tomorrow then it’s impossible to forecast, because everything’s going to be different.

- So the key to forecasting is to find something that will be the same tomorrow, and extend that to tomorrow.

- That something can be anything. I’ll give you a couple of examples.

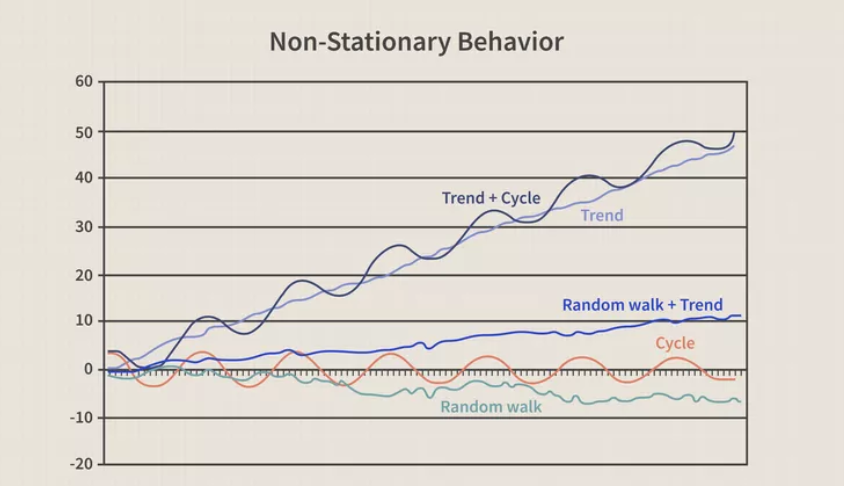

- If a time series is non-stationary (the stochastic component of) its distribution changes from time period to time period. With only one observation for each time period, it is difficult to see how one could make any inferences about the time series. It is like trying to hit a moving target knowing where it has been but with no knowledge of the direction it is moving in.

- Most of our statistical theory does not apply to non-stationary time series.

(5) Reason-5

- A stationary time series will have the same statistical properties i.e. same mean, variance and covariance no matter at what point we measure them, these properties are therefore time-invariant.

- The series will have no predictable patterns in the long term. The time plot will show the series to be roughly horizontal with constant mean and variance.

- Why do we need a stationary time series?

- Because if the time series is not stationary, we can study its behaviour only for that time period. Each period of the time series will have its own distinct behavior and it is not possible to predict or generalize for future time periods if the series is not stationary.

- A stationary time series will tend to return to its mean value and the fluctuations around this mean will have a constant magnitude. Thus, a stationary time series will not drift too much from its mean value because of the finite variance.

- One example of a stationary time series is ‘White Noise’. Cause of its inherent stationarity, it has no predictable pattern in the long term. It is thus memoryless.

- As you can see from the plot above, the distribution is constant across the mean and is completely random. It is difficult to predict the next movement of the time series. If we plot the autocorrelation of this series, one will observe complete zero autocorrelation. This means that the correlation between the series at any time t and its lagged values is zero.

- In the ACF (Autocorrelation Plot) above, you can see that all lags are within the highlighted area in blue. This indicates that there is almost zero correlation between observations at different lags. If one or more spikes are outside this range, or more than 5% of spikes are outside these ranges, then we can infer that the series is not ‘White Noise’.

(5) Example Of Stationary and Non Stationary Time Series

- Obvious seasonality rules out series (d), (h) and (i). Trends and changing levels rule out series (a), (c), (e), (f) and (i). Increasing variance also rules out (i). That leaves only (b) and (g) as stationary series.

- At first glance, the strong cycles in series (g) might appear to make it non-stationary. But these cycles are aperiodic — they are caused when the lynx population becomes too large for the available feed, so that they stop breeding and the population falls to low numbers, then the regeneration of their food sources allows the population to grow again, and so on. In the long term, the timing of these cycles is not predictable. Hence the series is stationary.